Implied Volatility¶

%matplotlib inline

import matplotlib.pyplot as plt

plt.rcParams["figure.dpi"] = 120

import numpy as np

from volkit import estimate_vol_from_option_prices

from volkit.datasets import spxw

Read Sample Data¶

We pick the options with an expiration date of 2 days, and at least 1 trade in both the call and put of the same strike.

df = spxw(min_volume=1, D=2)

T = df['T'].values

K = df['K'].values

F = (df['F_bid'].values[0] + df['F_ask'].values[0]) / 2

Compute 3 Implied Volatility curves: bid, ask, mid¶

# interest rate

r = 0.03

# Compute implied volatilies

iv_bid = estimate_vol_from_option_prices( df['C_bid'] , F, K, T, r, cp=1)

iv_ask = estimate_vol_from_option_prices( df['C_ask'], F, K, T, r, cp=1)

iv_mid = estimate_vol_from_option_prices( (df['C_bid'] + df['C_ask'])/2, F, K, T, r, cp=1)

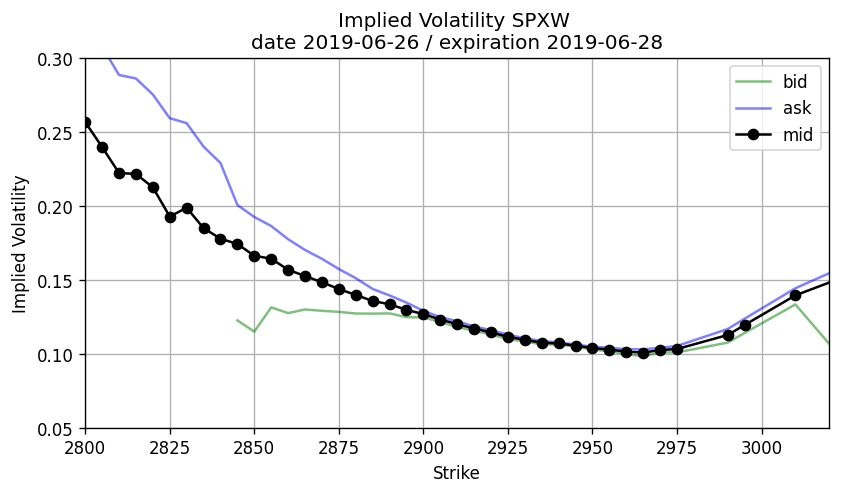

Plot the Implied Volatilities¶

fig, ax = plt.subplots(1, 1, figsize=(8, 4))

plt.plot(K, iv_bid, 'g-', alpha=.5, label='bid')

plt.plot(K, iv_ask, 'b-', alpha=.5, label='ask')

plt.plot(K, iv_mid, 'ko-', label='mid')

plt.xlabel('Strike')

plt.ylabel('Implied Volatility')

plt.title('Implied Volatility SPXW \ndate 2019-06-26 / expiration 2019-06-28')

plt.xlim(2800,3020)

plt.ylim(0.05, 0.3)

plt.legend()

plt.grid()

plt.show()