Implied Future & Discount From Option Prices¶

This notebook computes the implied underlying future from option prices of a single expiry.

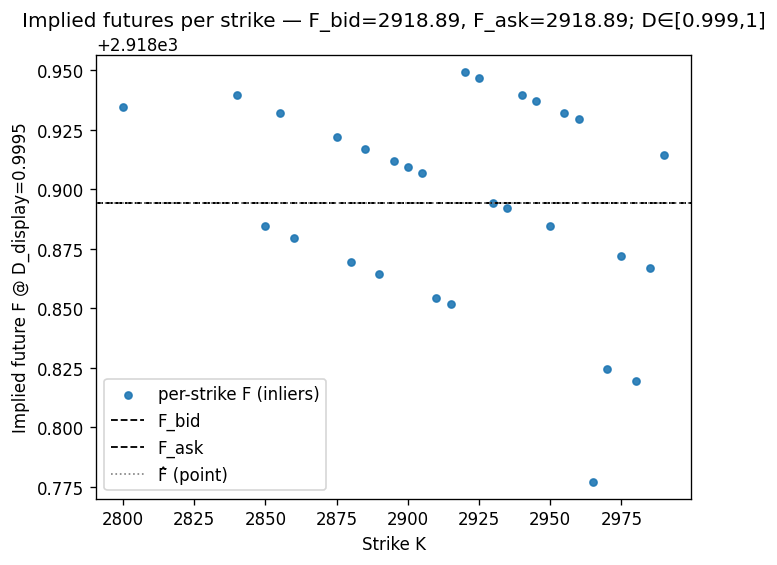

Computes an **implied future ** \(F\) and a discount range \(D\) that are jointly consistent with the quoted calls & puts.

Identifies and excludes the fewest possible strikes whose quotes prevent any consistent solution (likely stale/misquoted lines).

Visualizes per-strike implied futures.

%matplotlib inline

import matplotlib.pyplot as plt

plt.rcParams["figure.dpi"] = 120

from volkit import estimate_future_from_option_prices

from volkit.datasets import spxw

Read a set op example option quotes. Weekly S&P options with 7 days to expiry. Use only quotes that have been trades at least once (min_vol=1)

df = spxw(min_volume=1, D=7)

# Compute mid prices

C_mid = (df['C_bid'] + df['C_ask']) / 2

P_mid = (df['P_bid'] + df['P_ask']) / 2

res, valid_mask = estimate_future_from_option_prices(

df['K'],

C_mid,

P_mid,

plot=True

)

res

| F | 2918.894392 |

|---|---|

| F_bid | 2918.894392 |

| F_ask | 2918.894392 |

| D | 0.999803 |

| D_min | 0.99900000 |

| D_max | 1.00000000 |